There’s a new trend emerging among traditional enterprises who are going digital and embracing personalization. These enterprises are setting up innovation labs and digital teams as they gear up for what many are calling the ‘fourth industrial revolution’. One positive key trend to note is that customer engagement/satisfaction is a lead indicator. While top-line growth is a consequence.

Customer satisfaction is the key to evaluating enterprises

The change trickles down to how enterprises evaluate new products and offerings. There is a clear focus on customer-centric metrics. As opposed to purely revenue or cost-based metrics. Through Crayon Data’s work with one of the most innovative banks in Europe, and a digital bank in Asia, we were surprised to discover that quite a lot of emphasis is on customer engagement metrics. In fact, they were regarded as the key decision criterion.

For the European bank, driving activity on the platform along with a pre/post Net Promoter Score (NPS) measure were the key drivers to decision making. In the Asian bank, an NPS and a customer feedback survey formed the basis of evaluating us as a vendor.

To measure the relevance of a recommendation, we currently use engagement metrics like response rates, click-through-rates, and recommendation likes/dislikes. Applied specifically for banking, we nuance these metrics further by assigning a larger weight to engagement from at-risk, 30/60-day inactive customers. These metrics are heavily influenced by the channel of delivery, the UI/UX of the bank’s digital asset as well as the customer segments.

Net Promoter Score: what and why

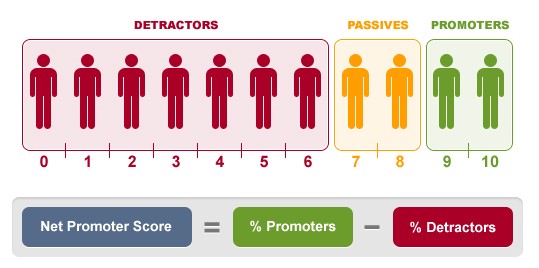

Net Promoter Score assesses to what extent a respondent would recommend a certain company, product or service to his friends, relatives or colleagues. But how does one measure it?

A customer/user is asked the following ‘ultimate’ question:

“How likely are you to recommend company/brand/product X to a friend/colleague/relative?”

By rating on a scale of 0-10, the respondents are grouped into promoters (those who scored 9-10), passives (scored 7-8) and detractors (scored 6 or less). Subtract the percentage of promoters from the percentage of detractors, and lo and behold! You have the Net Promoter Score. You can safely ignore the percentage of passives.

It’s fairly easy to collect. And even easier to interpret. A positive score indicates that your product, brand, company has a larger promoter base than a detractor base. The wide adoption of NPS is a consequence of this.

Is NPS fail-proof?

Not really. Let’s not get lulled by its simplicity. There are obvious challenges. The first one is cultural. For example, Americans are more comfortable giving extreme scores, while Asians prefer to be more moderate in their feedback. The second is selection bias. Frequent users/promoters are likely to be survey respondents.

More importantly though, at its core NPS measures “intent” to recommend and not the “act” of recommending itself. Consider the following conversation.

Employee: “We need to stop testing our product on animals!”

Employer: “But why? Shampoo companies do it all the time.”

Employee: “Yeah, but we make hammers!”

Funny as this is, it’s an example of what works for one, may not necessarily work for someone else. Similarly, the NPS system is not a one-size-fits all solution.

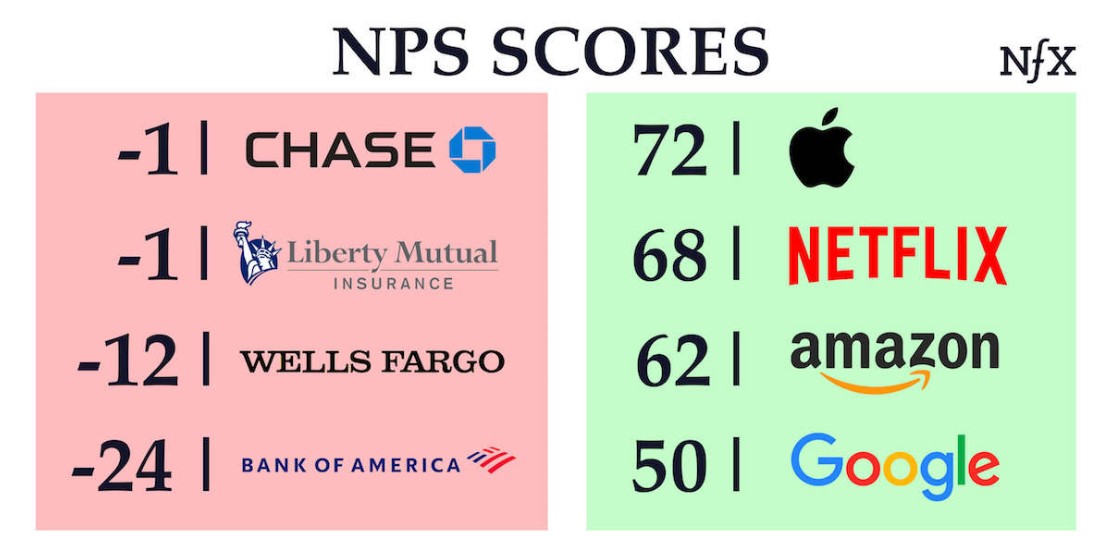

If we focus on the financial services vertical, NPS as a measure of customer satisfaction becomes even more prone to error. Some of these arise because, firstly, NPS might be rendered partially irrelevant in the face of data that depicts how consumers decide to change banks. Most promoters or detractors continue to face a high cost of switching banking services. Which is probably why banks seem to have sparse Net Promotor Scores compared to more digital savvy companies like Netflix and Apple.

Secondly, the cost of acquisition is high. Looking purely at a NET promoter scale would lead to a false sense of calm. As an example, a bank with 15% promoters and 5% detractors would have an NPS of 10. So would a bank with 40% promoters and 30% detractors. The cost and the focus for both would be entirely different.

According to a Wall Street Journal analysis, “net promoter” or “NPS” was cited more than 150 times in earnings conference calls by 50 S&P 500 companies in 2018. Of all the mentions the Journal tracked, no company ever said its NPS declined. This points to a deeper issue of treating NPS as a ‘vanity’ metric.

What does this mean for maya.ai?

As the core recommender engine to deliver personalized choices, Crayon makes customer engagement better.

There are other aspects to a digital experience encompassing UI/UX, widgets, etc. As we deal with an increased emphasis on customer engagement metrics, we are constantly working on benchmarks to quantitatively and qualitatively asses the relevance of our recommendations. We are also testing multiple processes to do so. Ranging from A/B testing to qualitative feedback from customers. The objective is to show that our personalized recommendations will add an incremental lift to the NPS scores.

Creating this database is critical as we move to build social proof points while riding the digital banking wave.