Co-authored by Manu Jeevan.

More than 70% of banking executives worldwide say that customer centricity is important to them Surprisingly, research by Capgemini indicates that only 37% of customers believe that banks understand their needs and preferences adequately. So these facts clearly show that banking executives need a deep understanding of their customer needs to achieve greater customer centricity.

This is surprising, given the increasing volume and variety of data that banks have about their customers. Customers frequently interact with their banks through mobile and website and, as a result, banks have a substantial amount of customer data. However, banks only use a small portion of this data to understand their customers. Research shows that less than half of the banks analyze customers’ external data, such as social media activities and online behavior and only 29% analyze customers’ wallet share (one of the main measures of a bank’s relationship with its customers)[Source: BBRS reasearch].

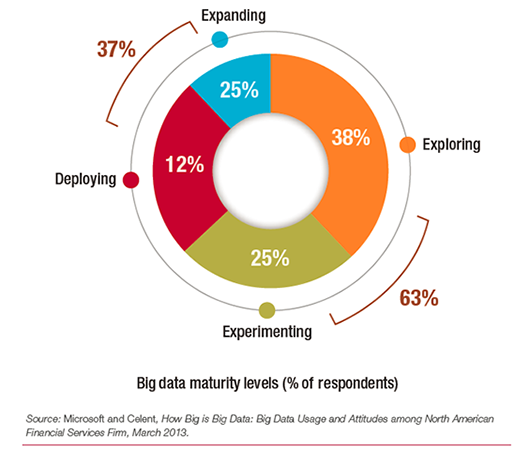

Over 60% financial institutions in North America believe that big data analytics offers them a substantial competitive advantage. Adding to this, over 90% believe that successful big data initiatives will determine the winners of the future [Source: Microsoft]. However, a majority of banks are still struggling to implement big data analytics technologies. Only 37% of banks have hands-on experience with live big data technology implementations, while the majority of banks are still focusing on pilots and experiments.

Big data Adoption levels in banks:

Let’s now delve into the problems banks face with big data initiatives and how they can capitalize on it.

Why are banks unable to exploit big data?

Data silos, lack of analytics talent, lack of strategic focus, privacy concerns are considered to be the biggest barriers to big data adoption by banks. Here’s why:

Data silos:

Data silos are separate databases or data files that are not part of a banks’ enterprise-wide data administration. In other words, data is typically distributed across systems such as CRM, portfolio management, loan servicing, etc. The data present in these systems are both structured and unstructured data (video, text, etc.). As such, banks lack a seamless 360-degree view of the customer.

Skills and development:

Banks need data scientists to develop their data capabilities. For instance, their data scientists should not only be well versed in understanding analytics and software, but they should also have the ability to communicate with decision makers. It seems that hiring data scientists is like hiring unicorns!

Three-quarters of banks don’t have the right resources to be able to gain insights from big data [Source: Ngdata]. Banks also face the challenge of training end-users of big data, those who aren’t data scientists themselves but need to use data to make decisions.

Lack of strategic focus:

Big data needs new technologies and processes to store, organize and retrieve huge volumes of structured and unstructured data. Banks still follow traditional data management techniques, which do not meet the requirements to handle big data. Likewise, most banks view data from a static and historical perspective. However, big data analytics are largely aimed to be used on a real-time basis. While most IT projects are driven by two aspects of stability and scale, whereas, big data demands discovery, ability to mine existing and new data, and agility [Source: MIT Sloan]. Consequently, by taking a traditional IT-based approach, organizations limit the potential of big data. In fact, an average company sees a return of just 55 cents on every dollar that is spent on big data[Source: Wikibon].

Privacy concerns:

The use of customer data raises privacy issues. [Source: Oreilly] Research indicates that 62% of bankers are cautious in their use of big data due to privacy issues. [Source: Monetizing payements, Ng data]. Outsourcing data analysis activities or distributing customer data across departments for gaining insights increases security risks.

For example, a security breach at a leading UK-based bank exposed databases of thousands of customer files. Although this bank launched an urgent investigation, files containing highly sensitive information — such as customers’ earnings, savings, mortgages, and insurance policies — ended up in the wrong hands[Source: daily mail]. Such incidents catalyze the concerns about data privacy and prevents customers from sharing personal information in exchange for customized offers.

Examples of how banks have solved their business problems using big data analytics

A survey conducted by Capgemini and EFMA indicated that risk management has been a high-priority area for most banks, while using customer analytics to enhance customer experience has been largely ignored.

Research shows that banks that implement customer analytics have a four-point lead in market share over banks that do not. The difference in banks that use analytics to understand customers is even starker at 12% [Source: Aberdeen analytics in banking].

Big data solutions can help banks generate more leads. Consider the case of a US bank. The bank wanted to focus on data coming from multiple channels to drive strategic decision making and improve lead conversions. So, it deployed an analytics solution that combined online and offline channels and provided a combined view of the customer. This integrated data fed into the bank’s CRM solution, supplying the call center with more relevant leads. It also gave recommendations to the bank’s web team on how to improve customer engagement on the bank’s website. As a result, its lead conversion rate improved by over 100% and customers received a personalized experience. The bank also executed three major website redesigns in 18 months, using data-driven insights to refine website content and increase customer engagement[Source: Adobe]

Assessing risks and setting the right prices are key success factors in the competitive retail banking market. Existing scoring methodologies, mainly FICO scores, assess credit worthiness, based solely on a customer’s financial history. However, to ensure a more comprehensive assessment, credit scores should also include additional variables such as demographic, financial, employment, and behavioral data. By using advanced predictive analytics, based on these additional data points, banks can significantly enhance their credit scoring mechanisms.

Although ‘current account’ balance levels and volatility are good indicators of financial stability, transaction drill-down analysis provides in-depth insights about customers. It enables the segmentation of customers, based on spending behavior. Startups such as Zest finance, Kreditech, LendUP and Lenddo are leveraging social network data to help banks analyze their customer data.

How can banks scale-up to the next level of big data analytics

To scale-up big data analytics effectively, banks have to stop seeing data as just an IT-asset. Rather, banks need to consider data as a key asset and move towards a model where analytics is an integral element of the decision making process across the organization. As a first step towards building expertise in big data analytics, banks need to establish a well-defined recruitment process to attract analytics talent. They need to also invest in continually training their analytics staff on new tools and techniques.

The quality, accuracy, and depth of customer data decide the value of customer insights. Consequently, banks will need to implement data management frameworks to handle the collection of structured and unstructured data.

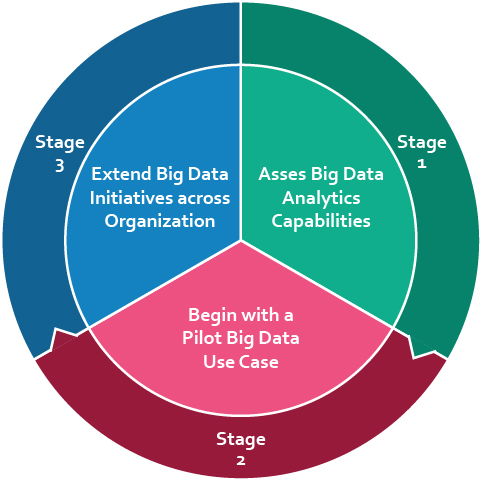

Big data initiatives are typically time and resource-intensive. To pave the way for smooth implementation, banks should follow a three-step approach:

- Assess existing analytics capabilities.

- Launch pilot projects.

- Expand the pilot project into full-scale organization-wide programs.

A capability assessment at the beginning of a big data program will provide banks with a view of the gaps in their systems, such as untapped data assets and key external data sets that are required to create a holistic view of the customer. These gaps might hold them back from adopting big data technology. With a clearer view of analytics capability gaps, banks will be better placed to prioritize their actions and investments.

Following a capability assessment, banks need to undertake their transformation journey in controlled steps, rather than in one giant leap. As such, banks should first identify and focus on a few small pilot projects, then use these as opportunities to test the efficacy of new analytics tools and techniques.

Conclusion

Implementation remains the biggest challenge towards the effective use of big data analytics by banks. While pilots deliver fast and measurable results, banks need to simultaneously lay the foundation to effectively scale-up big data initiatives. The key lies in adopting a holistic approach, where pilots are backed by a well-defined data strategy. The first step towards such an approach lies in changing traditional mindsets. Big data initiatives must be considered differently from traditional IT programs. They must extend beyond the boundaries of IT department and be embraced across functions as the core foundation for decision-making. Only then will banks be able to put the growing repositories of data to good use.