In recent years, the banking industry has witnessed a massive influx of raw processing power as well as data that is being analyzed through it. With the introduction of cloud computing and big data tools, financial institutions have it within their ability to do more with the analytics provided to them.

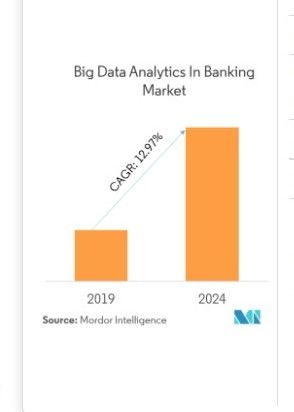

With the ability to produce massive amounts of data, analytics can help financial institutions explore opportunities and improve customer experience through efficient decision-making. Thus, data analytics is driving the banking/financial sector. This is illustrated by the graph be

Many organizations are taking advantage of the perks of data analytics, but at the same time, there is a risk involved. The truth is that some actions are erroneous and render data analytics as invalid.

Here is what banks and other financial institutions want from their data analytics.

- quick access to numbers

- all operations need to be data-centric

- be informed and ensure that decision-making is improved with analytics

The domino effect in data analytics

The problem with errors in data analytics is that it makes for a domino effect. You will find that when you get the analytics wrong, the advanced innovation, the open APIs, and the customer journey —everything goes awry.

Other factors hold banks from fully utilizing the potential of data analytics. For instance, banks may cherish customer data, but they do not fully comprehend how to use this data in the application. It should not just end at a consumer report but be used to come up with innovative solutions.

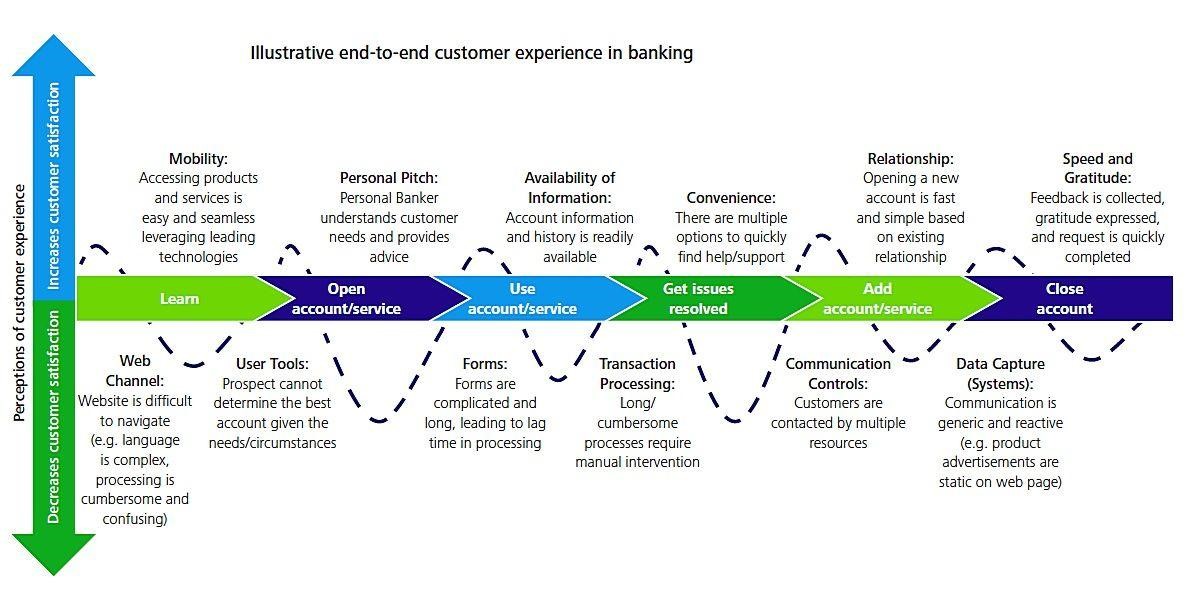

The benefits of data analytics are that it improves the customer journey, ensures a real-time personalized experience, and improves efficiencies and productivity. The goal is to raise revenues for banks.

Data analytics mistakes that banks make

There are specific barriers to correctly using data. Also, there are mistakes that financial institutions make when using data analytics. Here are some of the most common ones.

Starting data analytics without an objective

The right step to data analytics is making sure that you know two things:

- exactly what metrics you want to track

- what value you must derive from these metrics

A lot of banks offering services such as working capital loans or leasing options continuously try to improve the customer experience, but they are not even equipped with the basic conversion tracking setup. Thus, they fail to achieve factors that drive these results.

This problem occurs when banks fail to set a specified objective for their analytics. It is plain and simple — how can a bank get the answers it seeks when it doesn’t even know what it’s looking for?

At its core, data analytics help optimize marketing endeavors of a business, so it’s a brilliant way to address business concerns and adds value to banks. The objective could be anything, from tracking conversion rate to the average service order value of the bank.

Too much misinformation out there

It could not be any truer. With an excellent hype for data analytics and an increase in usage, on the vendor side, it is extremely crowded to the point that it becomes not only overwhelming for the banks but also confusing.

Banks make the mistake of giving in to the complexities of it without understanding it first. It is incredibly important to realize that data analytics can be and is, in fact, more straightforward than what many vendors make it out to be.

If a bank wants to use it in the application process of customers, it must understand the procedure first. The new action should be to ditch the problematic toolsets that the bank unnecessarily plans to invest.

Not enough governance of data

Part of this problem lies in the pseudo complications of data analytics. There is too much control given to different approaches. What the banking industry needs right now, is to put into effect standardization policies.

Without standardization across the data ecosystem, banks are left with only a PowerPoint presentation to back it up.

Working on a grand scale

There is a higher chance of mistakes when you are dealing with data analytics on a bigger scale. Since everything is so magnified, when people think it would make it easier, it gives more room for risk.

It takes time to sample, test, document, and plan. If a bank skips any of those, it must pay a hefty price.

Doing it the DIY way

We have already established the fact that data analytics is super crowded. Banks have a whole department set up for people who write the code from scratch, then there are those who check the code, and then, testing is done for the code they wrote in-house.

Let’s not forget that many professionals need an open source code when it comes to quality assurance, which leaves much responsibility on the department’s shoulders.

Not only is this inefficient, but it also increases the risk of employing data analytics in banking strategy. A bank’s best bet would be to eliminate all possibilities for errors. There is a more straightforward way to go about it.

There are plenty of tested professional tools available in the market with a track record of providing excellent data analytics. Not only will they save time and money, but they will also streamline the process for banks, with minimal risk involved.

Create reports with no value

In the banking industry, the best way to go about data analytics is to export every figure derived from the tool employed in a compiled report. With massive data volumes, banks must cope with infiltrating the data, which is the most common mistake of all. In the end, you are creating the report just for the sake of reporting the numbers.

The theme of every report should be what questions they raise and how these questions can be answered. Every report must add more value to the operations of the bank. The chart below reveals that data analytics is used 35% for reporting purposes at banks.

The novel idea is to make a report that addresses the current banking concern. If there are metrics that do not answer business questions, they should be left out. You should not fall into the trap of camouflaging additional data as relevant.

Becoming a creature of algorithm habit

One thing that works for every financial institution is that they realize that there is no algorithm out there that will work for every single situation for a bank. You cannot get the information from a single data source.

It is easy to find convenience in a single data tool, but that does not mean that this tool should be used for everything. The bank wastes money and at the same time boosts the turnaround time.

It is essential for banks to explore new data solutions; they must be useful rather than expensive. The best way to go about this is to calculate its total cost to the banking organization and the value it provides.