Yesterday’s technology is tomorrow’s trash. That’s how fast tech is evolving. But around the world, regulatory and public-policy decisions are made in silos. People are overlooked.

That’s why there’s an ongoing wizard fight between tech innovators and policy makers. Should tech evolution lead to policy revisions? Or should policies support continuous tech innovation?

Back in 2018, the Saudi Arabian Monetary Authority (SAMA) had a simple solution. Let them figure it out in a regulatory sandbox. They invited local and international firms to test new digital solutions in a ‘live’ environment. And by January 2021, the Kingdom of Saudi Arabia (KSA) was able to announce their Open Banking Policy.

‘KSA’s 2030 Vision’ links directly to SAMA’s Sandbox.

One of the main objectives of this vision is to reinforce economic growth and investment activities by

Supporting entrepreneurship

Enhancing fintech services

Creating responsible banking ecosystems

Engendering financial inclusion

In SAMA’s sandbox, entrepreneurs can leverage facilities and play around with new solutions. Without regulatory obligations bogging them down. The experimentation phase helps set guardrails before deploying to customers.

This is a creator’s dream! Teams can test their solutions in a controlled environment before taking them to market. They also receive support and guidelines through SAMA advisors.

The freedom for creative exploration and experimentation has had multi-dimensional benefits.

Innovators have:

Championed groundbreaking innovations and new technology

Scaled existing technology

Reduced time to market for firms

Fostered partnerships

Meanwhile, policymakers have received evidentiary support in decision-making, effecting regulatory change. They have also acquired deep and wide-ranging insights that will help them understand and test existing frameworks.

For customers, this means better financial products and services. And increased privacy. While companies are in the sandbox, customers have full control over their personally identifiable information (PII). In these experiments, data is securely shared with third-party providers only after seeking customers’ explicit and informed consent.

Innovators are also required to provide clarity to customers by:

Providing clear statements indicating their participation in a test

Providing valid permissions acquired from SAMA.

Indicate the cap on the number of users and transactions for each experiment

Seven fintechs were part of the first SAMA sandbox cohort in 2018. By 2021, the number had grown to 18.

They were categorized under

Buy Now Pay Later

Digital Payments

Debt- Crowdfunding Platform

Consumable Micro-Lending

Digital Savings Associations

Financial Information Aggregation

Digital Savings Solutions

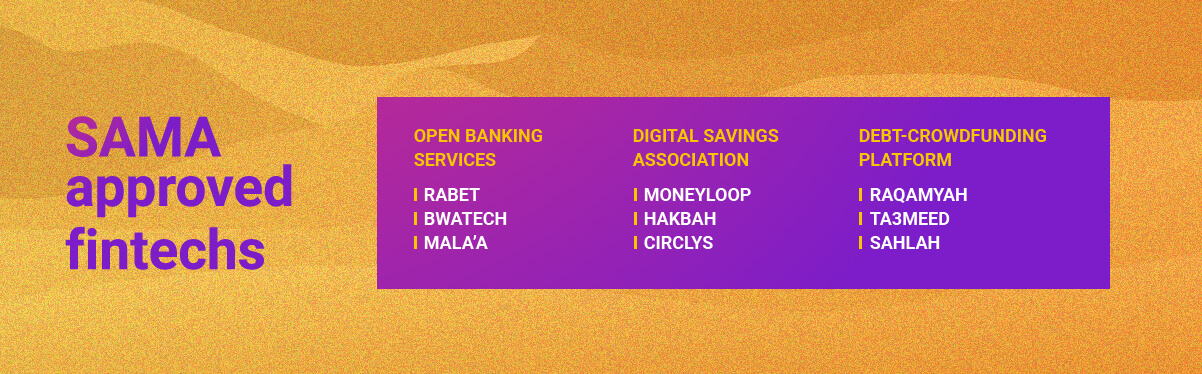

Currently, SAMA’s official site lists nine permitted fintechs. In January 2022, Rabet Financial became the first company to secure regulatory permission for its open banking solution. Bwatech and Mala’a followed closely in March 2022. Earlier, in 2021, SME crowdlending platform Raqamyah raised a 2.3 Mn USD investment to help comply with SAMA’s full license requirements. And Hakbah, a savings app, raised 1.2 Mn USD in seed funding after receiving SAMA approval in 2020.

Overall, the regulatory sandbox in KSA is a win-win-win. For innovators, regulators, and customers. It’s an ongoing model to follow, and emulate, anywhere in the world.